US Military Could Boost Silver Demand

By Renu Singh

Summary

- Silver, based on Silver Wheaton’s latest results were below the mark, aggravating the company’s weak financial performance.

- Driven by industrial demand and silver production, the price of the metal is expected to increase, and this will have a positive impact on Wheaton.

- Being a streaming company, Wheaton doesn’t need to invest in mines, which is an advantage since it can focus its cash flow on signing more mining agreements.

- Wheaton will also benefit from an expected uptick in gold pricing, as it has bought additional gold streams from Vale.

The recently reported fourth-quarter results of Silver Wheaton (NYSE:SLW) didn’t bring any joy to investors, as its revenue and earnings declined massively on a year-over-year basis. In addition, Wheaton missed analyst estimates. In fact, Wheaton has fallen short of analysts’ earnings estimates in three of the last four quarters.

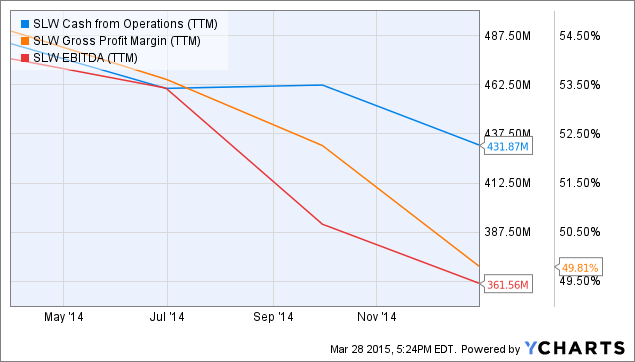

However, as I had pointed out in my earnings preview, investors should not expect a quick turnaround at Wheaton, as the increase in price of gold and silver will take some time. As such, it is not surprising to note that Wheaton’s key metrics have been on the decline in the past year as shown below:

SLW Cash from Operations (TTM) data by YCharts

What next?

In my opinion, investors need to take a longer view of things, as Silver Wheaton’s performance depends a lot on the price of silver. The good part is that Silver Wheaton is a streaming company, which means that it doesn’t own any assets. Rather, the company enters into agreements with other mining companies, and purchases their production at a fixed price, which is ideally lower than the market price.

As such, the company doesn’t have to incur any development of capital expenditure costs. In fact, this business model is a smart one since Wheaton can pay “low predictable costs for precious metal streams from a diverse portfolio of high quality mines.”

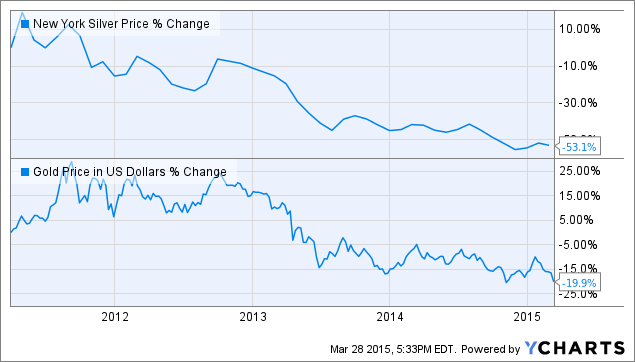

Thus, in the end, the company’s performance boils down to metal pricing and Wheaton’s streaming arrangements. As such, it is not surprising to see why the company has underperformed the market in the last four years, losing almost 60% of its value since April 15, 2011. The prices of both silver and gold have dropped massively in the past four years as shown below:

New York Silver Price data by YCharts

But, this trend is expected to change going forward on the back of increasing demand for silver. According to a Gold-Eagle report:

Silver’s total industrial demand is forecast to grow 27% through 2018, meaning an additional 142 million ounces of silver will need to be supplied.

Despite price weakness in 2014, which inspired a lot of badmouthing of precious metals in the financial media, silver coin demand hit new records. The U.S. Mint sold more than 44 million Silver Eagles, up from 42.7 million the prior year. At one point last fall, the dysfunctional government mint had to suspend orders because it couldn’t keep up with demand.

As demand for silver increases, so will the price as miners are currently controlling production. As such, it is not surprising to note that Silver Wheaton’s bottom line will increase at an impressive CAGR of 20% over the next five years. Source:

Call Us Today Toll-Free 888.747.3309

Request a FREE Silver Report on How to Protect my Assets

Related posts