God’s Words of Strength to His People During Financial Turmoil

Summary

- The recent developments in Russia may also play a role in the progress of GLD.

- The upcoming non farm payroll report could bring further down GLD.

- Let’s examine the relation between GLD and U.S. dollar.

By Lior Cohen

The price of the SPDR Gold Trust (NYSEARCA:GLD) declined by only 3% during 2014. Nonetheless, the ETF also recorded an 11% drop in

its gold hoards, as investors continue to exit the gold ETF. Will the recent developments in Russia play a role in the progress of the GLD price? Let’s also examine the relation between the U.S. dollar and gold and the upcoming non-farm payroll report.

Russian gold

The recent plunge in the price of oil has been weighing in on Russia. The country heavily relies on oil and oil related products – they account for roughly two-thirds of the country’s exports.

Some news outlets already suggested that Russia could start to sell off gold following the drop in its cash pile – this is due to the plunge in the Russian ruble that instigated a capital flight.

Up to now, the country has been buying gold while the rival from the west – Ukraine has been cutting down its gold holdings to finance its war efforts.

As a result, during the past few months, Russia has increased its gold hoards as indicated in the chart below.

Source of data: Gold Council

The higher demand for gold may have partly contributed to the resilience of gold prices to remain relatively flat throughout most of the year.

If Russia does plan to start selling off its gold hoards, this could have a modest adverse impact on the GLD price.

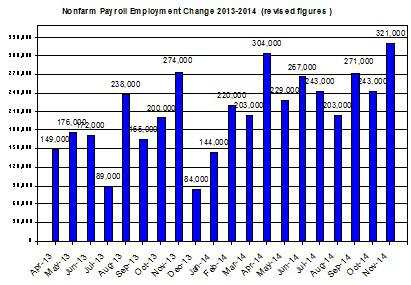

Looking forward, the main event for next week is the U.S. non-farm payroll report. During most of 2014, the employment reports were very good and even beat market expectations. This news tends to negatively relate to the changes in the price of GLD.

Source of data: Bureau of Labor Statistics

If we were to see another strong non-farm payroll report that will exceed market expectations, this could bring further down the price of GLD.

The relation between GLD and the U.S. dollar

I would also like to make a quick note about a recent interesting article I came by, in which the author makes the point that GLD isn’t related to the changes in the U.S. dollar. While I agree that the relation between GLD and the U.S. dollar isn’t reliable, may vary over time, and doesn’t necessarily imply causation; I still think that the progress in the U.S. dollar does correlate with GLD and should be considered.

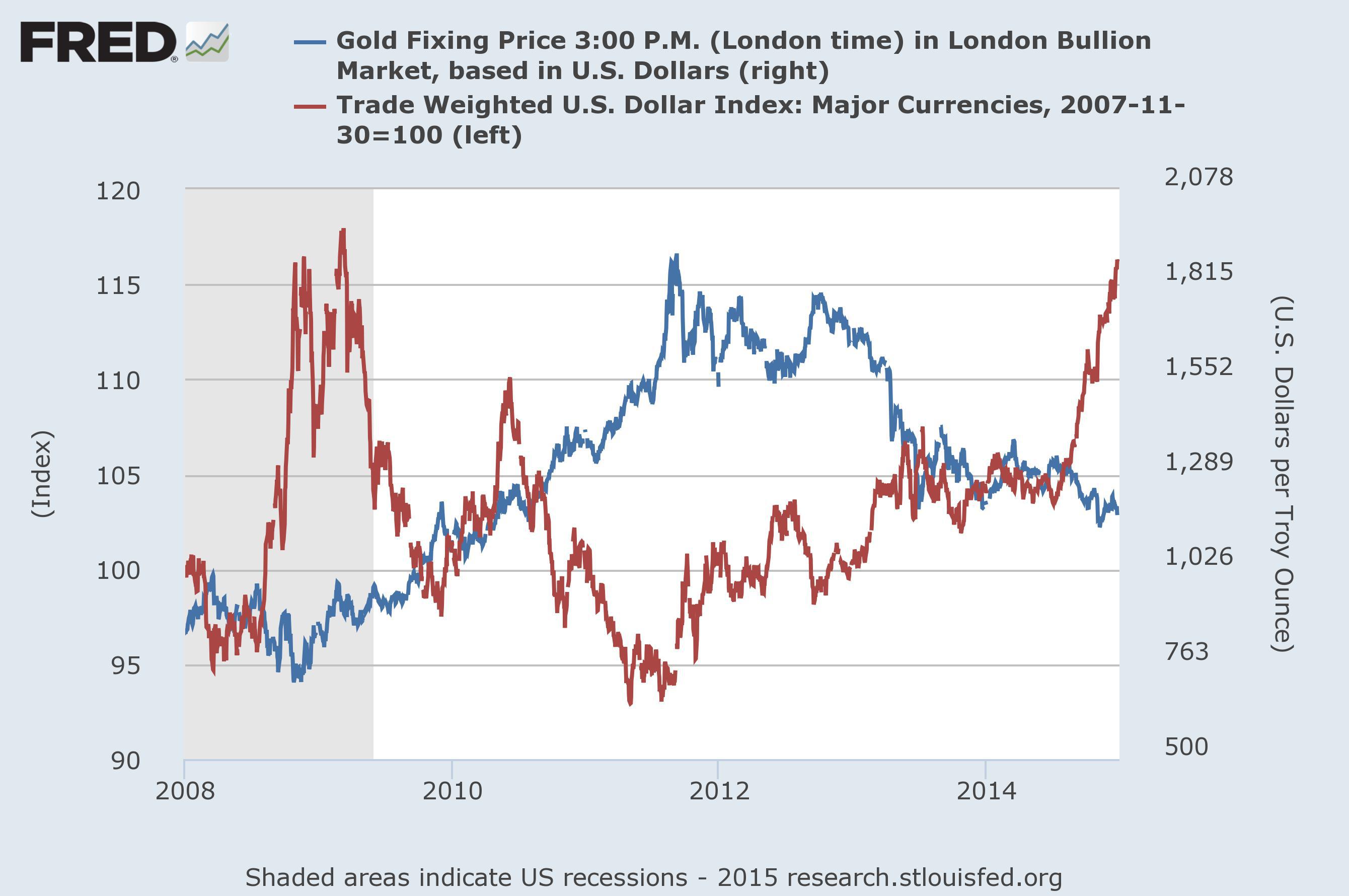

First, let’s review the progress of U.S. dollar and gold over the past few years.

(click to enlarge)

Source of chart: FRED

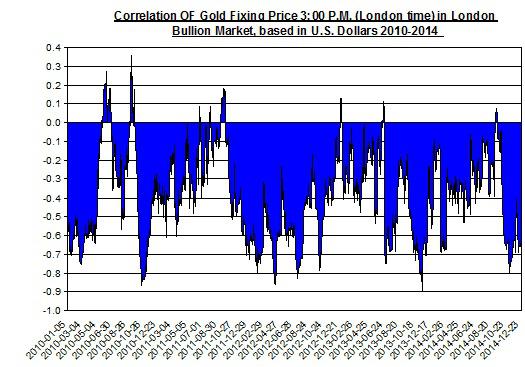

The chart doesn’t provide a clear picture about the relation between the U.S. dollar and gold. But if we were to examine the relation between the daily percent changes of two data series over the last four years, then linear correlation is -0.38. Further, if we were to examine the linear correlation (moving average over 20 business days) between 2010 and 2014; then we could see that while the correlation isn’t consistent as it varies over time, for the most part the correlation is mid-strong and negative.

Source of data: FRED

During these years, we had several factors that may have impacted both GLD and the U.S. dollar, including changes in inflation expectations, the Federal Reserve’s monetary policy, and the changes in the U.S. and global economic stability. Also, we had other factors that may have impacted one data series but not the other, e.g. the changes in the CME’s margin requirements had a strong adverse impact on gold prices but little effect on the U.S. dollar.

These events don’t negate the relation between the U.S. dollar and GLD, rather only point out the limitation of this relation.

What about the rise in gold miners’ productions costs in recent years? Will this pressure up the price of GLD in the near future?

Major gold producers such as Goldcorp (NYSE:GG) and Barrick Gold (NYSE:ABX) are already starting to adjust to the low gold price environment as they have been cutting costs: Goldcorp’s all-in sustaining costs reached $920 per ounce of gold this year – roughly 18% lower than last year; Barrick Gold’s AISC also fell by 8% this year to $844 per ounce.

This could suggest a slower growth in gold producers’ yield in the coming years, as they limit their production to assets that provide a positive ROI under the current low gold prices. This isn’t, however, likely to play a significant role in the price of GLD anytime soon.

As I pointed out in the past, the price of GLD is more likely to be driven by the changes related to the demand for gold on paper rather than the changes in demand and supply for the physical metal.

GLD could see additional losses in the near term. If the U.S. dollar keeps recovering, and if the U.S. non-farm payroll report shows another strong growth, then these turn of events could correlate with the downfall of GLD. Source:

Call Us Today Toll-Free 888.747.3309

Request a FREE Silver Report on How to Protect my Assets

Related posts