God’s Words of Strength to His People During Financial Turmoil

Summary

- Stocks are so overrated.

- Stocks have their meaningful place in a long-term investment strategy.

- But so too do many other investment alternatives.

Stocks are so overrated. Don’t get me wrong – I love the stock market. The opportunity to conduct fundamental analysis on publicly-traded corporations to identify potential ownership in high-quality businesses trading at attractive valuations is the reason why I decided to pursue a career in the investment industry so many years ago. But when listening to people in the media and elsewhere talk about capital markets, stocks are so revered above all else that one could easily include that no other choices exist out there to invest your money. But while they have their place, and I typically have a fairly meaningful allocation to them myself, they are far from the only game in town when it comes to investing your money.

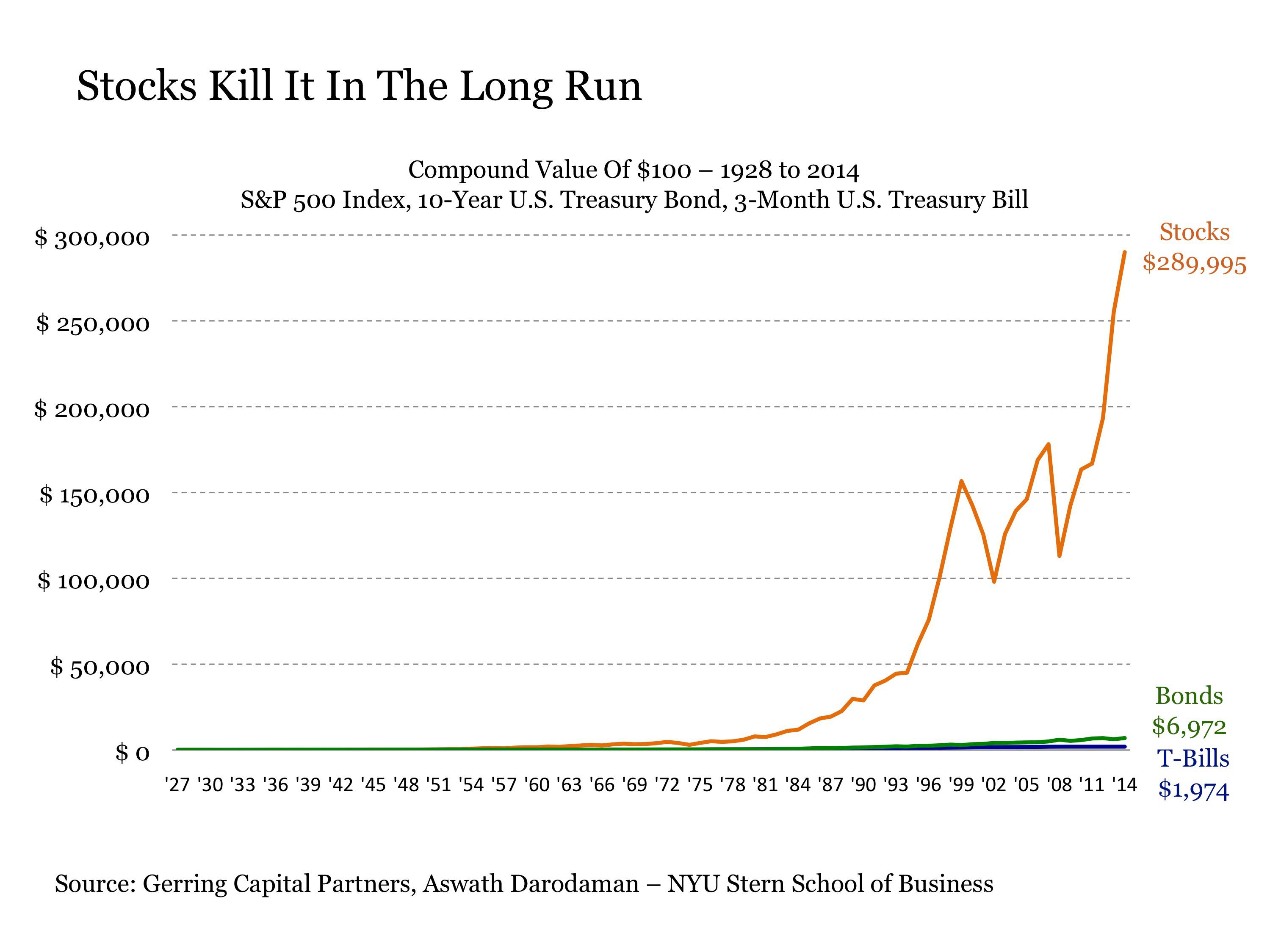

Stocks Absolutely Kill It In The Long Run

At first glance, the case for stocks looks like a complete and total slam dunk. In short, if you have any reasonably long period of time before you need your money, perhaps as little as a few years, one should have most if not all of their investments allocated to the stock market to maximize the growth of capital. One has to look no further than the experience in investment markets over the past 87 years dating back to 1928. For if $100 was invested each in the S&P 500 Index, 10-Year U.S. Treasury Bonds and 3-Month Bills at the beginning of 1928, the value of these investments by the end of 2014 would be $289,995 for stocks (NYSEARCA:SPY), $6,972 for bonds (NYSEARCA:IEF) and $1,974 for T-bills (NYSEARCA:BIL). Given the magnitude of this difference, it would be more than reasonable to conclude that one should put all of their long-term investment money into stocks. Quod erat demonstradum.

But . . .

Not so fast. Here’s the first problem that immediately presents itself. It’s great that stocks have done so well since 1928, but I don’t have an 87-year time horizon to invest. In fact, nearly all of us have a much shorter time horizon. As a result, I need to be a bit more sensitive to some of the things that might happen along the way over this 87-year time horizon to make sure that I can meet my goals sometime before then in the time horizon that makes the most sense for me.

Another issue also hangs out there that grabs my attention. For about the first 60 years of this chart from the late 1920s to the late 1980s, the three lines on this chart are all fairly close together. It’s not until the late 1980s that stocks leave the competition behind. We all get the power of compounding and the big swoosh to the upside it provides in the later years of a long-term time horizon, but 60 years is a long time to wait for this big payoff. And perhaps there are some considerations that I need to explore more closely in the trip along the way for stocks in the event that I might want to access my money sometime less than 60 years from now.

What Have You Done For Me Lately?

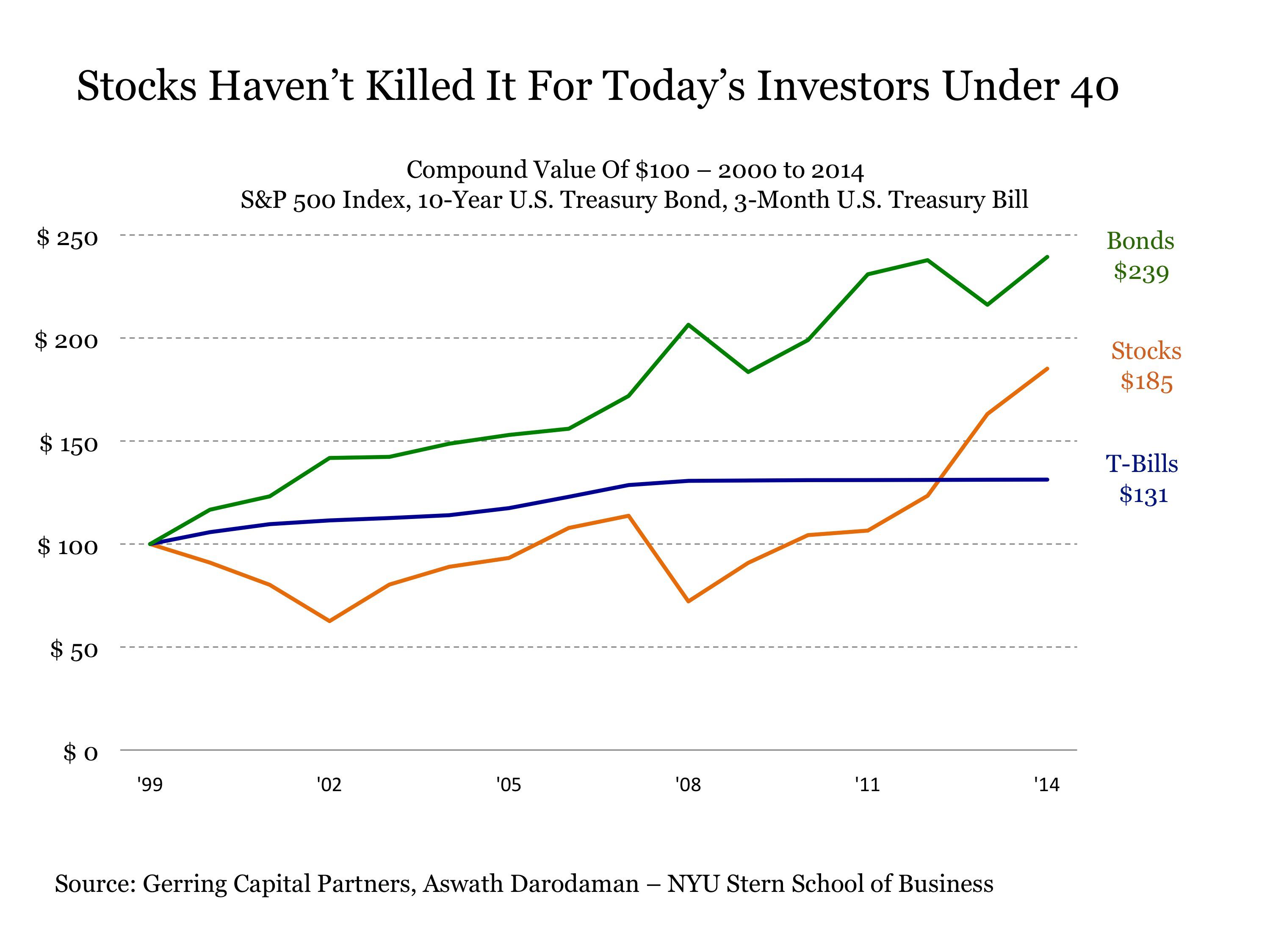

So given these first two time horizon issues, I need to take a closer look to see if stocks are really as dominant as they first seem. Naturally, my next step is to take a look at what the typical investor experience has been in recent years. We live in a “what have you done for me lately” world after all.

What then, for example, has been the investment experience of the typical person under the age of 40? These are people that graduated from college starting in the late 1990s and likely got started investing in the markets with the start of the new millennium. With all of the Baby Boomers now retiring, what this group thinks about investing is particularly important as they will be the ones putting their money into the market to help offset what the ballooning number of retirees will be taking out in the coming years (this assumes, of course, that the U.S. Federal Reserve and other global central banks someday actually get out of the endless money printing game – I wish I could say with certainty this is actually going to happen).

So what has been the experience of the under 40 crowd? They have experienced two major stock market crashes where they have seen the value of their investment evaporate by more than half. And if they managed to keep their job during the financial crisis by taking a hefty pay cut in the few years that followed or find a decent job that paid them reasonably well sometime in the aftermath of the financial crisis, this was not likely the group that was ready with dry powder to deploy in the stock market at the March 2009 bottom. In other words, many probably missed a good deal of the latest bounce that has defied gravity over the past six years. And even for those who were fully invested throughout this entire time horizon, they would have seen their investment in the 10-Year Treasury bond perform nearly twice as well as their investment in the stock market. If fact, these investors would have done better by simply keeping their money in cash until 2013 when the Fed went all in with QE3 and increased their balance sheet by more than 50% with $1.6 trillion in asset purchases. Thank God, all of those asset purchases helped spark the sustained economic recovery that so many in this younger generation are benefiting from today. Oh yeah, it didn’t.

Was It Good In The Beginning?

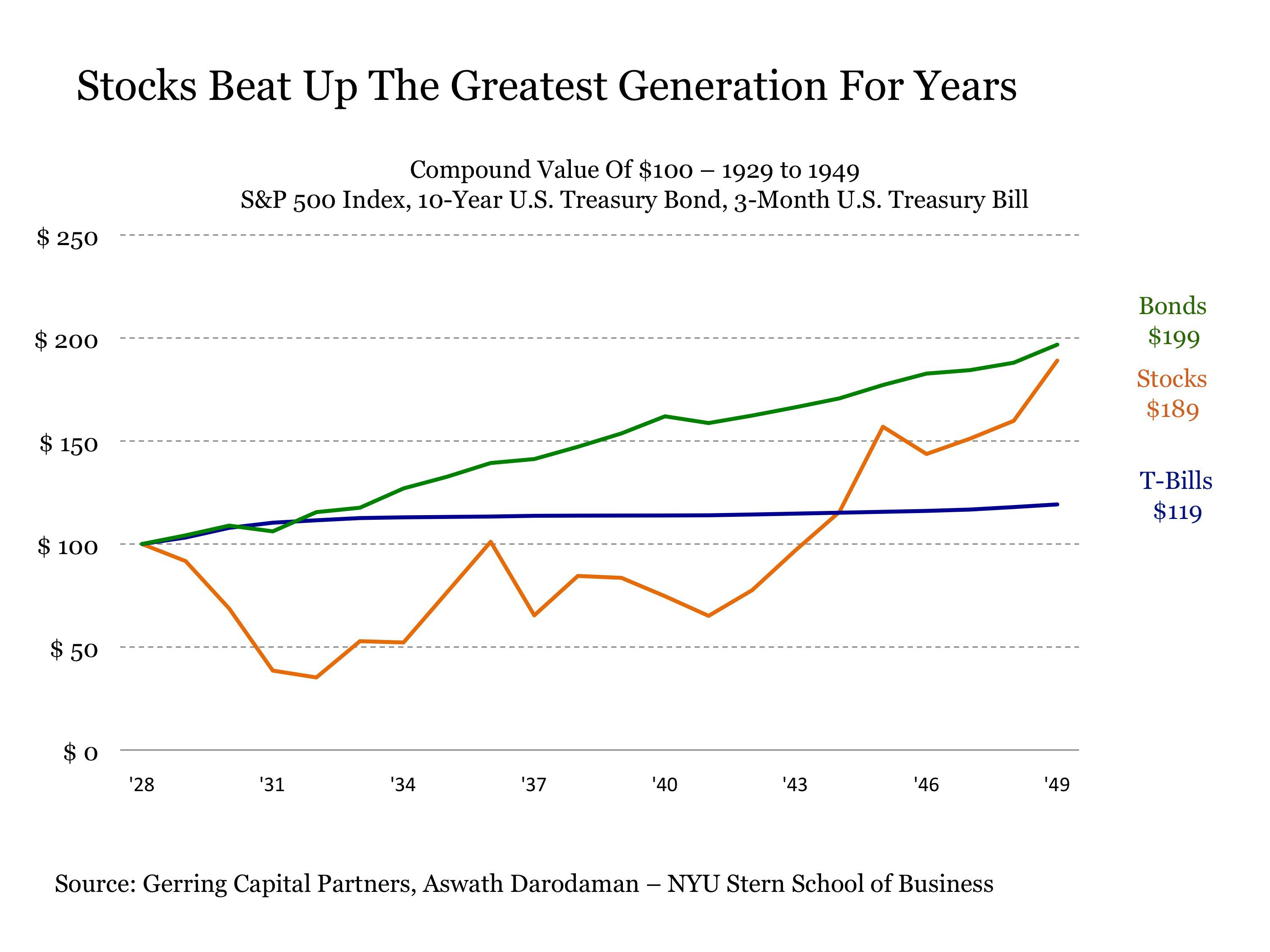

So if stocks have generated such lackluster results over the past 15 years, which makes up one-sixth of our entire 87-year time horizon, where exactly did the payoff take place over time that gave us such great results for stocks?

It most certainly was not in the beginning. For if we think that the under-40 crowd today has had a tough time with stocks, just ask someone who was getting started in stocks back in the late 1920s. Back then, it was just plain ugly for the young stock investor. This was the time when my late grandfather for which my company Gerring Capital Partners is named was first getting started in the stock market. And he was the exception to the norm for many in the Greatest Generation that simply came to the conclusion as they aged that “stocks cannot be trusted as an investment.” Obviously, this opinion was shaped by their experience in their formative years of investing.

Here we have another generation of investors that for a two-decade period saw the value of their 10-Year Treasury bond steadily rise and eventually double while at the same time their stock investments were essentially underwater until the end of World War II a decade and a half later where they would have been better off keeping their money in T-bills instead. And while my grandfather purchased his first 100 shares of General Electric (NYSE:GE) in 1933 roughly a year after the 1932 market bottom, he by his own admission was the rare exception to the norm in doing so at the time.

What About In The Middle?

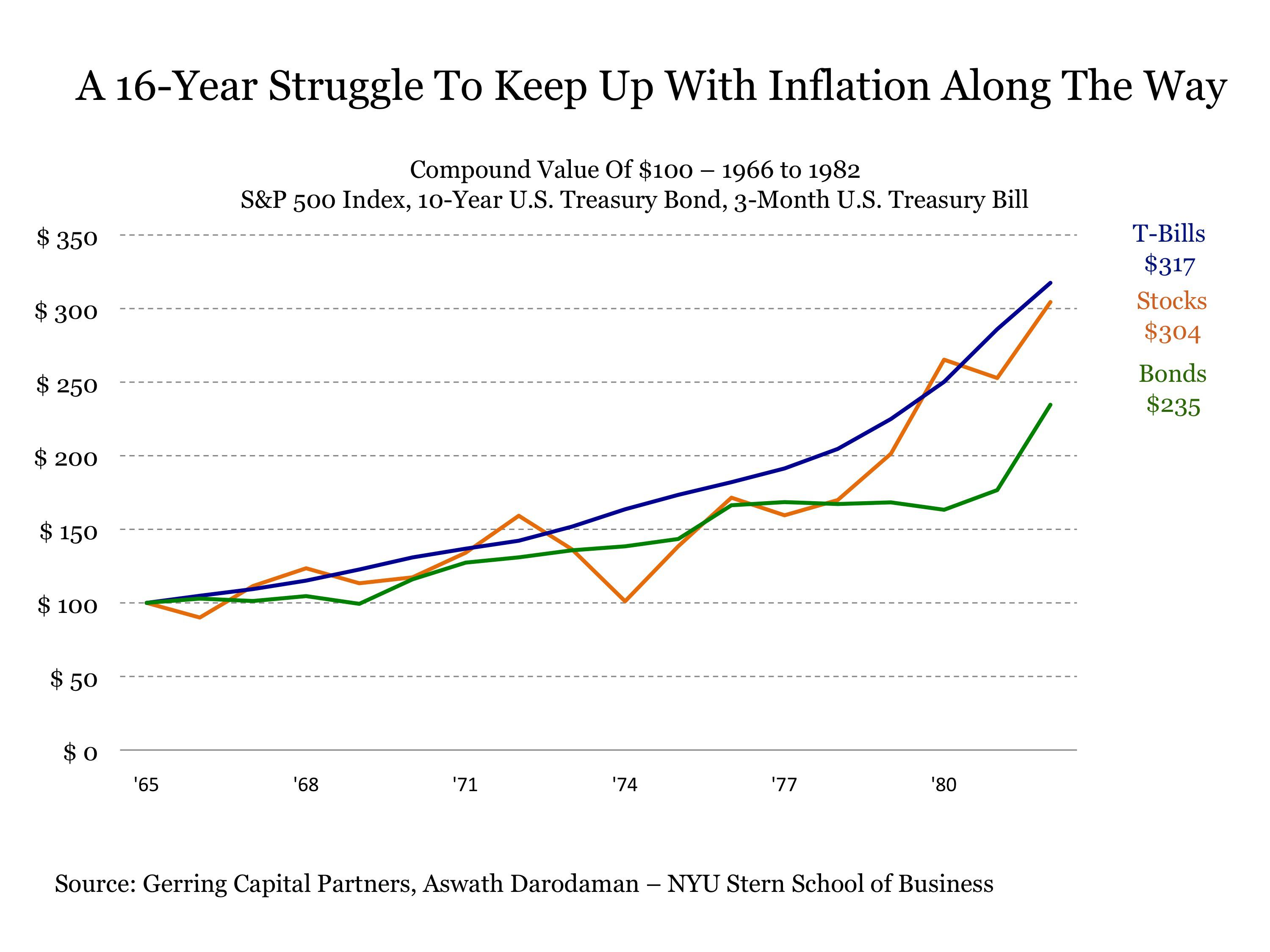

OK. So we’re now up to two-fifths of our entire 87-year history where stocks have generated less than stellar results. Stocks were lousy in the beginning, and they’ve been lackluster toward the end of this time horizon. The big payoff must have come all along the way in the middle then, right? Not necessarily.

Let’s consider the generation of investors that were getting started in the stock market in the mid-1960s. This includes the late end of the Silent Generation and the early Baby Boomers. For nearly the next two decades, these investors aren’t necessarily getting killed in stocks, but they aren’t killing it either. Neither are they doing very well in bonds during this time period. In fact, the best performing category from 1966 to 1982 was none other than cash (gasp!) in the form of 3-month T-Bills. The fact that cash was the best performing asset class over this time period reminds us that while stocks and bonds may have been making money on a nominal basis during this time period, they were losing value on an inflation-adjusted basis. Source:

So Where Then Is The Juice?

Call Us Today Toll-Free 888.747.3309

Request a FREE Silver Report on How to Protect my Assets

Related posts